Speed read

War in the Middle East is a real risk. But the market’s whipsaw recently is also a familiar reminder: geopolitical shocks often produce more noise than lasting damage. Prices move fast because uncertainty moves fast. Attempting to predict short-term headlines is rarely a reliable investment strategy. Over the long run, the bigger risk is often not the headline itself, but reactive decisions that interrupt compounding. A diversified portfolio is built to withstand moments like this, and the evidence consistently favours discipline over drama.

Key takeaways

-

Geopolitical shocks tend to create fast market moves, not permanent damage. History shows an initial drop is common, but recoveries often follow once uncertainty clears.

-

Oil is the transmission mechanism, but supply buffers matter. OPEC+ spare capacity is a meaningful shock absorber, and scenario outcomes depend heavily on whether the Strait of Hormuz disruption becomes sustained and enforceable.

-

History shows that selling during periods of stress has often resulted in investors missing subsequent recoveries, which can meaningfully reduce long-term outcomes.

What's happening

It is natural to feel unsettled when conflict escalates in a region as central as the Middle East. When oil prices jump, markets wobble, and the news cycle turns up the volume, investors instinctively ask the same question: what does this mean for the plan?

That concern deserves a straight answer.

Markets have faced episodes like this before. Many times. History does not provide certainty, but it does provide perspective on how these periods typically behave, and on what tends to help, and harm, long-term outcomes.

What matters most

In the immediate aftermath of the latest escalation, Brent moved sharply higher before settling back into a lower range. Equity markets fell briefly and then partially recovered. That pattern is not unusual. Markets reprice uncertainty quickly, then wait for hard information.

The key variable is not the headline. It is whether oil supply is materially disrupted, and whether any disruption is temporary or structural. On that front, the numbers matter. Current analysis points to OPEC+ holding roughly 2.8 million barrels per day of spare production capacity. Iranian exports were last estimated at around 1.6 million barrels per day. In other words, there is capacity in the system to cushion an outage, assuming shipping routes remain workable. US shale also provides flexibility that did not exist in earlier decades.

If the Strait of Hormuz disruption proves temporary and conditions normalise, Brent could drift back down from elevated levels. If the situation remains ambiguous, prices can stay higher for longer. A full, enforced and sustained closure is the true tail risk, and it is the one scenario that could push prices sharply higher, but it requires a very different set of conditions.

The takeaway is simple: the market is not guessing. It is pricing a range of outcomes.

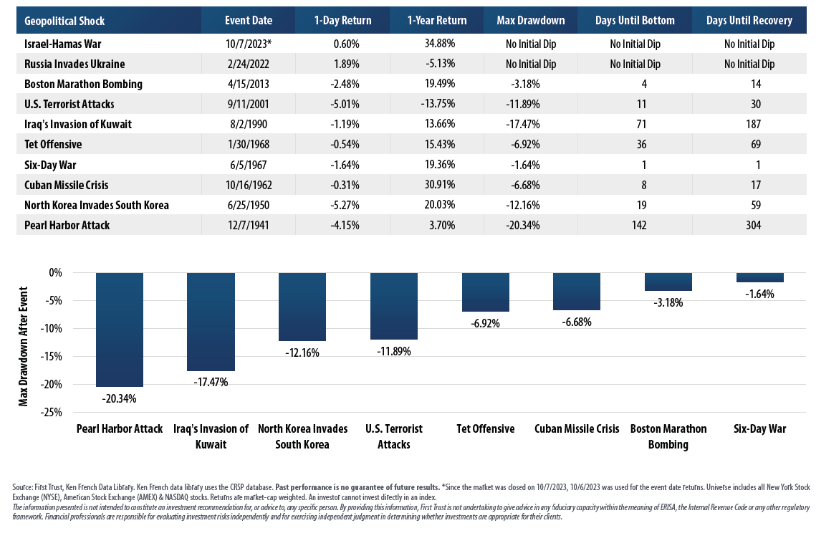

What history shows

There is a consistent sequence in major geopolitical shocks involving energy markets: an initial sharp reaction, a period of uncertainty, then stabilisation once the real economic impact becomes clearer.

Chart 1: U.S. stock market returns after major geopolitical shocks (first trust)

One analysis of geopolitical shocks since the Second World War found the S&P 500 typically fell on day one, experienced a modest peak drawdown, and recovered within weeks rather than years. Twelve-month returns were positive in most cases.

The 1990 to 1991 Gulf War is a useful example. Oil rose sharply, equities fell materially, and then markets recovered within months. By the end of 1991 the S&P 500 had delivered a strong positive return. Investors who held through the discomfort were rewarded. Investors who sold into the decline locked in the damage.

The important counterexample is 1973, where an oil shock collided with embedded inflation and a very different policy backdrop. That period reminds us that not every episode is identical. It also reminds us to distinguish between a temporary spike and a structural shift.

What investors get wrong

The trap is that uncertainty feels like a call to action. Selling feels prudent when the news is frightening, and buying back feels sensible once things “make sense” again. The problem is that markets tend to recover before the story feels safe. Most investors do not miss the bottom because they are slow. They miss it because they are waiting for emotional permission.

The market is at its most uncomfortable precisely when information is at its worst. That is why decisions made in the middle of a crisis tend to be decisions made with incomplete data, elevated emotion, and a very short time horizon. They may feel prudent in the moment, but they often turn temporary volatility into permanent shortfall risk.

This is not theoretical. The cost of missing the recovery can be large because rebounds are often concentrated into a small number of trading days. If you are out of the market waiting to “feel better”, you are usually waiting for prices to already be higher.

The real risk to the plan is not a scary month. It is making a decision during a scary month that permanently lowers the chance of meeting long-term goals.

What we do about it

A well-built portfolio is designed for exactly these environments. Diversification across regions and asset classes is not a slogan. It is the practical acceptance that shocks happen, cannot be timed, and should not be allowed to dictate the long-term plan.

At PortfolioMetrix, investment management by design means we build portfolios to withstand uncertainty and we manage them with discipline, including rebalancing when markets move. We focus on risk, the risk of not meeting long-term goals, rather than treating volatility as a signal to abandon a plan that was sound before the headlines arrived.

The current situation warrants attention. It does not warrant panic.

Staying invested through uncertainty is not passive. It is an active decision to let time and compounding do their work, even when the news is trying its best to convince you otherwise.